theDirt Monthly: Heat Waves

August 2023

Down and Dirty

The year-over-year trend is fewer closings, lower prices, slight increases in inventory, and longer time on the market.

The Trend is your friend

Central Texas is smack dab in the middle of a terrible trend. We’ve recently broken the ‘running days of over 100 degree heat’ record. The last record was set in that other terrible drought year of 2011. One looks around and all the vegetation is brown and dormant or heading that way. Even the trees are starting to give up. At the ranch, we haven’t had rain since June. And the paltry moisture in that month amounted to all of 0.52 inches. That’s it. That’s all. I’ve sold all but a handful of the cows. The ones remaining are on meager rations. There just isn’t enough of anything to feed them. And I look at the weather every morning and see almost the same thing that all of you see… no end in sight. Equities people say the trend is your friend but there is nothing friendly about this trend.

My kid asked me the other day when it would all stop. Even the young and normally oblivious are gob-smacked by this infernal hell of a heat wave. My bitter, sarcastic answer is that this is the new normal, that we are now the Kuwait of America1, and that it will never rain again. Gallows humor I suppose. But the truth of the matter is that all trends end. This too shall pass. The ocean temperatures and jet streams that collude to make this heat wave will be interrupted by the catalyst of summer changing to fall. Then fall to winter. Surely - SURELY! - the changing of the seasons will interrupt the weather gods in their mischief and force them to change tack.

Longer than you think

I’ve written previously about my notorious inability to estimate the time of my projects. I can plan and anticipate and even budget a fudge factor but no matter what, something comes along to knock the card castle down and extend my project timelines by weeks (sometimes into infinity). I’ve come to accept it so it is no longer (as) exasperating. As a result I have this life rule that it will usually take longer than you think2.

So it goes also with the economy and markets. One puts all the puzzle pieces together, reads the tea leaves, and develops a hypothesis. One thinks, ‘Surely - SURELY! - things will make a turn and soon’. Then the economy trudges on day after day, week after week, month after month. Plodding along in the same old fashion. A trend, if you will. And absent some massive and very powerful catalyst (global war, Pandemic, the Fed going on an interest rate bender, etc), the economy and markets can roll along in terrible ignorance of fundamentals for a long, long time before the anticipated change occurs.

As a very Dirty and very Nerdy person, I very much enjoy the quarterly reports of Dr. Lacy Hunt. Within finance and economics circles, he is something of a celebrity and guru. He’s got a Ph.D in Economics3. He used to work at the Fed. And he has been at this finance game for around 40 years or so. And he’s been opining about the economy for all of that time. He probably understands the mechanics of the economy as well as anyone. In July, he did an interview on a podcast/ finance nerd show called Wealthion in which he prognosticated about the economy. It is well worth the watch/ listen. He also publishes a quarterly newsletter which is free for all to read. I highly recommend it: https://hoisington.com/economic_overview.html. In both the interview and the report, Dr. Hunt describes how the economic system lags the financial system by about 6-9 quarters (approximately 1.5 to 2 years). Essentially he expects that the decisions and actions of the Federal Reserve to take that long to shake out in the real world. Guess what? We are about 7 quarters in from the start of monetary tightening policy.

Does this mean that something will change tomorrow? Nope. Next quarter? Nope. The answer is nobody knows. Just like I thought that this year would be a good year for rain because last year was less then 20 inches and that has never happened two years in a row based on 124 years worth of rain data… the universe can and will conspire to disappoint you. Black Swans and such.

The point, Dear Reader, is that long-range weather forecasts and timing the market have always been undertakings that will make a fool of the smartest of humans. Trends can plod along for quite some time. Will it change? Will the heat wave end? Will the downward pressure on real estate prices stabilize and reverse? Yes. Of course. As sure as summer turns to fall turns to winter every year, the trend will turn. It’s just that you just can’t count on a firm date. And it will probably take longer than you think.

Markets in July

Economic fundamentals remain absurd: the short term price of money is higher than the long term price of money (aka the yield curve is inverted). The Fed remains committed to reducing inflation: the target federal funds rate is now 5.5% after the FOMC hiked another 25 basis points in July. So the trends of interest rate increases looks to continue. This does not bode well for real estate. Currently, the cost of a prime 30-year conforming mortgage hovers near 7%. Less-secure real estate loans (like land loans) are closer to 10% for the prime borrower.

The current real estate market is defined by demand constrained by rising interest rates and increasingly difficult financial underwriting. This in the face of slightly increasing but still constrained supply. There isn’t much (if any) distress on the sell side and many who are on the fence about selling are choosing to wait it out. The end result is a continued mildly downward pressure on prices across the board. Buyers with cash are still king, cash is moving markets, and there appear to still be plenty of dollar bills at work. Enough to make a market anyway. Sellers who prefer to move quickly and who market their properties ahead of the downward trend will likely sell within 180 days. Those who think it is still 2021 and market as such will see their properties languish on the market with many “price improvements” in their future (see below)4.

Data on Acreage Property Listings in the Central Texas area

As of the day that I crunched numbers (August 6), there were 2,319 acreage properties5 active on the Austin MLS (this includes those marked as Active under contract and Pending) in the Central Texas area (currently defined as 120 miles from my house). This is a 11% increase in inventory of acreage properties from this time last year. Of those 2,319 acreage properties currently on the market, 769 (33%) have decreased their price at some point over the course of their listing. Of those, the median6 price change is about an 8% decrease and the average is 12%. These figures track with the over 11.2% decline in house prices in the Austin MSA.

Of the acreage properties currently on the market, 1,994 (86%) have been on the market for more than 30 days; 1,682 (72%) have been on the market for more than 60 days; and 816 (35%) acreage property listings have been on the market for more than 180 days. Of the acreage listings that have decreased their price at some point during their time on the market, 401 (17%) have been on the market for more than 180 days.

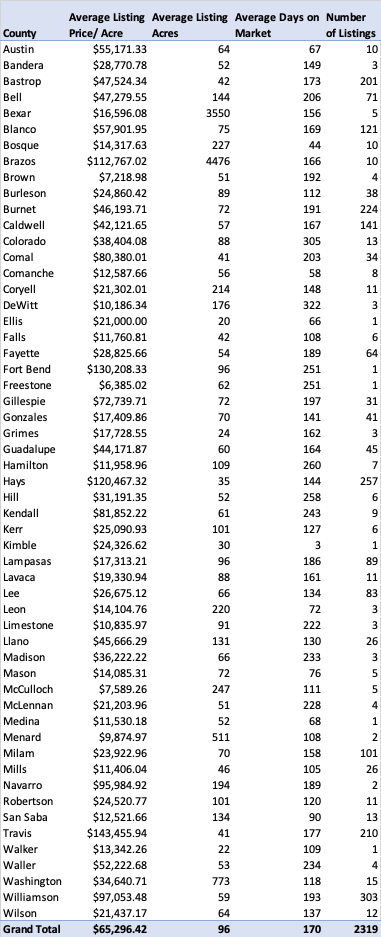

Here is acreage property listing data information by county (from ABOR):

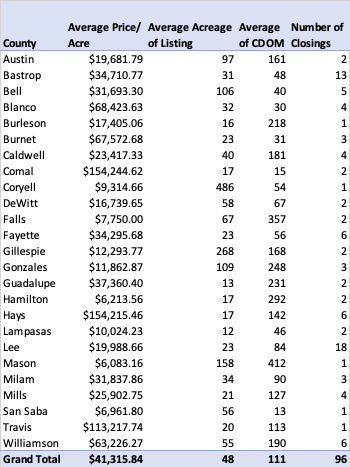

Last, but not least, July closing data -or- ‘where the buyer meets seller and the rubber meets the road’

There were 96 closings for acreage properties in July. This is down 20% from the 120 closings in July 2022. The average close price per acre for all counties is $41,315 which is down, you guessed it, 12% from $47,039 in July 2022. The average Days on Market has increased 31 days from July 2022.

So… the trend is fewer closings, lower prices, slight increases in inventory, and longer time on the market. See you next month.

A hot and HUMID desert. A see of brown. One of the most miserable places I’ve ever seen.

This, of course, invites the corollary rules: Enjoy the journey; and Be content in the struggle.

Maybe a bona fide, maybe not depending on who you ask.

Also known as ‘death by a thousand cuts’.

I define acreage properties as those 11 acres or more.

I like to look at median here because there are bad data points and outliers that can skew an average. Keep in mind that for median, half of the price changes will be more than the median and half below.