theDirt Weekly: December 17, 2022

Predicting: The Fool’s Game

Down and Dirty this week

Inflation is cooling. But is still high at around 7.1% year over year.

The Fed increased its funds rate by .50 points to a target rate of 4.25% - 4.50% and signaled more increases to come.

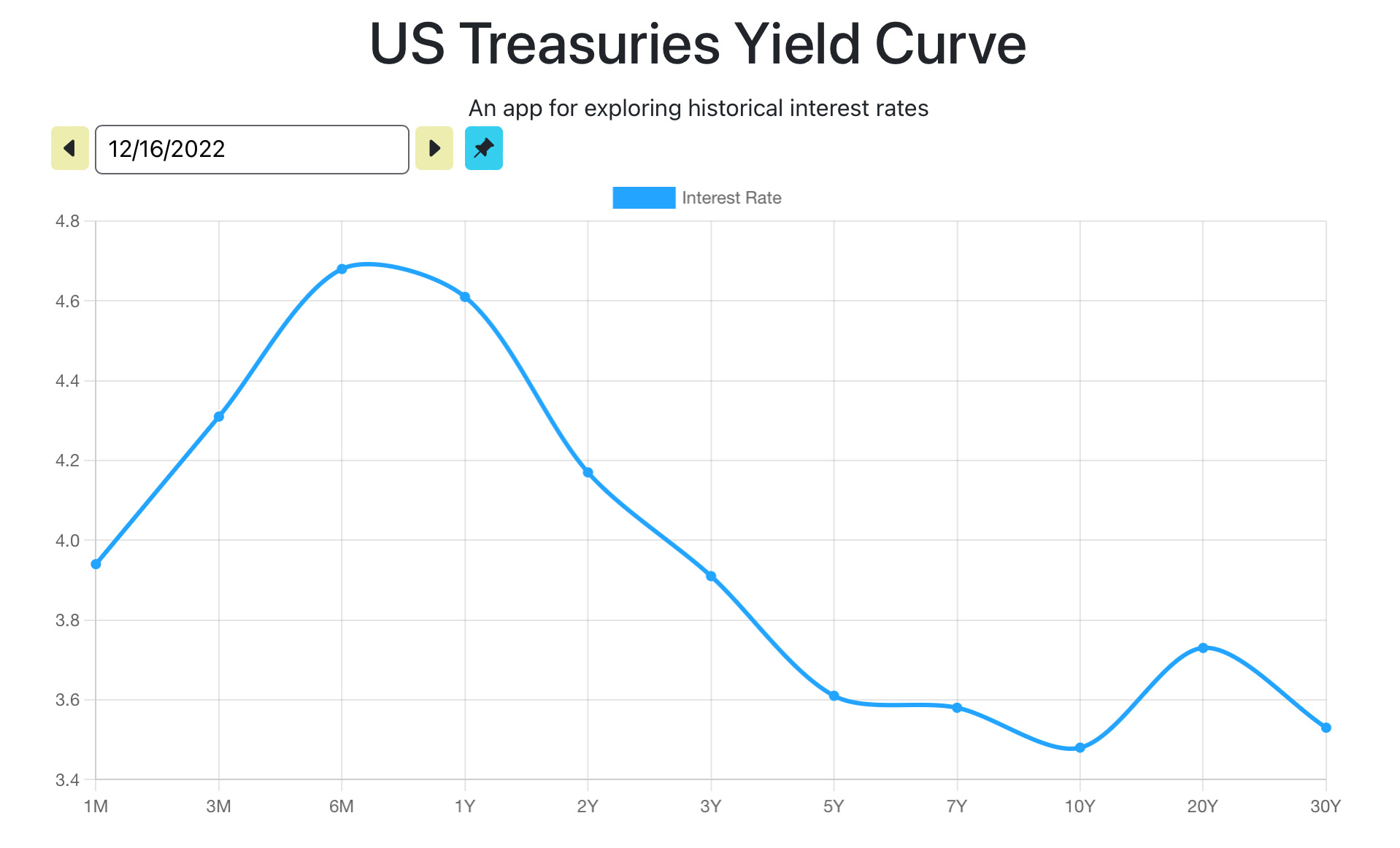

Stock markets took a hit on recession fears. 10-year treasury rates decreased (ironically in the face of Fed funds increase thereby easing mortgage rates and, perhaps, downward pressure on real estate prices)

Bad news keeps pouring in. But the beatings will continue until Uncle Jerome is satisfied.

Elections are over and the new regime turns to making new laws: Farm Bill, Texas Leg agenda, etc

Predicting: The Fool’s Game

I enjoy playing chess. Many years ago and when I was new to the game, I recall laying out in my mind the exact moves I would need to make to take a queen or a knight. If I move here then my opponent moves there then I move here, etc. But the game never quite unfolded the way I wanted. That was more true the more complex and specific my plan and also the further into the future (the more moves) that I planned. And that’s true because the opponent also has a plan and a goal and a move and he or she almost assuredly wants the opposite of what you want (it is a binary game of win-lose, after all). And so my well thought out strategies and plans blew up in the face of reality. Every time. Why couldn’t it ever just work the way I wanted? It was all very frustrating for the novice chess playing version of a much younger me. Fast forward to today.

The way I played chess back in those days reminds me so much of the allure of predicting the future today. It is all so much linear thinking. If the Fed does X then CPI will do Y and real estate will do Z. If I buy A property and do B then I can sell it for C. But experience will educate; especially experience gained after taking a hairy risk and falling flat. Indeed experience will chasten. And I, dear reader, have previously been chastened. I’ve been humbled and shaped by the fiery forge of fickle reality. In the past my plans have been crushed; my hopes smashed. And then looking about in the rubble, the house of cards that were my assumptions laying crumpled on the ground, I felt stupid. I felt like a fool. So it goes when you hold on too tight to a specific outcome in a vast ocean of possible.

I’ve been reminded of this these past few weeks as I work with a client to place funds into real estate assets that will, hopefully, produce a decent return over time. But we are in a period of transition and change that makes judging a jump from one rocking boat to another especially difficult. And in my reading this week, I am reminded to not think too hard on one specific outcome. Because we live in a complex system and the future is a range of possible outcomes and dependent on infinity variables and circular arguments. And so the wise investor hopes for the best. And plans for the worst. But what precisely is the worst?

Will we experience a nasty recession next year as the Fed goes too far with monetary policy? Definitely possible. Will we experience a light recession after a Fed pause but marked also by stubbornly high inflation figures and an equally stubborn labor market? Such a case is highly plausible. Will the Fed, caught in a debt trap of its own making, pivot too soon and mire us all into a realm of high inflation and no growth? I heard the argument and nodded along. Dear reader, I’ve no idea what will happen. Maybe none of these things? Maybe all of them? Maybe something completely different that isn’t being discussed and cannot be imagined? Probably. But I just do not know.

I can’t and won’t write that one ‘shouldn’t make assumptions’. Assumptions are a part of life, and there are certain broad assumptions we all must make going forward. We must have a thesis. And the broad thesis under which I march forward into tomorrow is that the rule of law will hold. Private rights will remain (mostly) intact. And our economic system and Culture of Exchange will evolve and change but function well enough to allow us to get by much the way that we’ve been getting by for thousands of years. Hell, some of us might even prosper.

And only a bit more specifically: I propose that we are headed sideways with lots of inflation in the future as our world reorganizes. I think the price action of the 1970’s is relevant. I believe that is a framework sufficiently narrow on which to act but broad enough to not be pigeonholed. So yes I assume. And yes I predict to a point. But I try not to predict too hard lest I once again look the fool. I try also to leave a large margin of safety for the inevitable margin of error. And I try to be open to all the ways in which I am wrong: and I know that there are, and ever will be, plenty of ways in which I am wrong. To err, after all, is divine.

With this stark mindset I scroll the tweets and the news and consume all the endless noise and jibber-jabber (to which I also now contribute). I listen to podcasts. I read lots of substack articles and a few books. All the while hoping for revelation and some sense of security. But there is none to be found. Only a vast range of possible. The more I read, the more unsure I become of any specific future. Dear reader, all I know for sure is the present. And the following is what I know today:

Our Current System

We are a Credit Driven Economy: this is especially true for real estate. Easy credit drove prices up. Restrictive credit now drives them down. The data here are clear. It is a highly causative relationship. We are all at the mercy of that terrible god: the interest rate.

The American Dream

The American Dream of homeownership is alive and thriving. Owning a bit of Dirt runs deep into our souls. This inherent demand is not curbed at 6%+. Could that desire, that deep want for a place of one’s own, ever be curbed? I think not. The demand for house and home burns, rages really, within all of us. Much like lust. Or envy. Or greed. It’s baked into the animal and you ain’t gettin’ it out.

The Fed can only suppress the ability to act on that demand. They might skew the market with mixed signals of price. They might contribute to its excess or scarcity with flawed policy from on high. But the minute that levee breaks, a wave of desire will flood the market. Perhaps it was better to not dam the river at all. But we are too late for that now.

Also baked in

Combining those points, our real estate system is further defined by the reality of government insured and assured credit via quasi-governmental entities (Fannie Mae, etc) and the resulting collateralization of bulk debt products like Mortgage Backed Securities. The rules and laws and culture behind this great big mess are so baked into the system now that we can’t and won’t get it out. There will be no law tomorrow dispelling the MBS or CDO as mechanisms for pushing paper and distributing money and assets. Doing so would cause the entire house of cards to collapse. So we are now dependent on this system as the alcoholic to his ethanol.

Pushing Paper

And pushing paper (not really even paper anymore but imaginary 1’s and 0’s stored in (on?) so many Amazon servers) is the fact of our system. Our economy, our money, the markets have ever only been man-made and imaginary mechanisms for exchanging resources. They have been and are now governed by laws and contracts that are just figments of our imagination. I am going way down the rabbit hole now but think about it: what separates one nation from another? What separates my house from my neighbor’s? A fence? An imaginary line? A contract? And what if I smash right through them? Well the might of governments (which is just an organized representation of popular will, at least theoretically) will crush me and enforce the contracts. The Matrix runs deep, folks. Culture, belief and paper rule our lives.

So Average Jane can’t now afford a house in Austin that she could 10 years ago because her FICO is below 600 and her income is too low for a 6% FHA mortgage because Uncle Jerome decided to bump interest rates by a few points over the summer because he neglected to do it earlier because inflation was transitory and so house prices spiked but now the housing market has come to an abrupt halt and Average Jane is just screwed because we just gotta get inflation back down to 2% because mandates created by economic understanding from decades past. But the house still exists. And Average Jane’s desire to own the house still exists. Tis but a thin wall of imagined concepts like prices and money and interest rates stand between them.

It’s a strange old world when you dig deep, ain’t it? Which leads me to…

Fed Hikes and Antagonistic Effects

The Fed hiked the federal funds rate by 50 basis points this week. And the 10-year yield subsequently… fell. Which actually slows the downward pressure on real estate prices and so too the downward pressure on CPI. An antagonistic effect is a pharmacological phenomenon where a medication has the opposite effect to what is normal or intended. Such is the result of a very non-linear and complex system. And it is why, given multiple billions of variable inputs, specific predictions and outcomes are foolish and predicting itself so damned hard.

I wonder aloud the repercussions of the Fed completely losing control of interest rates (and money?). Especially the 10-year Treasury upon which so many mortgages are based. What if they hike and hike and hike the short term rate and the 10-year just falls and falls and falls. What if markets just… stop listening to the Fed and do their own thing? Control is a fickle mistress. Ideas and culture run deep but they are not impossible to change. A diktat from on high is only in force as long as the masses are willing to believe it has force.

John Wake: real estate in the internet age

I read a fantastic account by John Wake of his experience with how the internet changed the housing market and how that defied his predictions (and expectations). If you are a Dirty Nerd then I highly recommend the read: The Internet Made the Housing Market Less Rational.

I’ve also thought on this topic (over thought probably) over the last couple of years. I’ve come to the conclusion that the velocity and democracy of information (efficiency of information) has amplified our emotions within economic decision-making. In other words: the internet really let our crazy out. There are those who will decry the internet age and wonder what has become of us. I take another view: the crazy has always been there. It was just hidden by a lack of ability to efficiently communicate it. Now it’s on full display and we don’t particularly like what we see.

For real estate our desires are now magnified through the internet lens. The velocity and magnitude of price swings, that thing called volatility, is now a part of the system. Get used to it, it is here to stay.

We who call ourselves real estate professionals are required to adapt. Is six months of marketed housing supply “balanced”? Probably not anymore (if it ever was). What we thought about real estate for the past few decades will inevitably change. What was normal yesterday is no longer the case today. It is a Brave New World.

Wealthion podcast: demographics and labor

I listened to an intriguing podcast about demographics and labor. Wealthion: Record Millions of Adults Giving Up on Ever Finding Work. The down and Dirty is that there are a lot of people, especially prime-aged males, in this nation who are just refusing to work. Is this so much click-bait? Or is there something to it? I am not sure yet. But as I wrote in last week’s Dirty Thought about railroads, I believe that we face a massive Human Problem when it comes to labor. It seems an inflection point. And it seems very inflationary.

Human Problems: the Fed fiddles with numbers while real people burn

I’ve read, listened, and thought a great deal about how our economic system, our Culture of Exchange, has evolved over the past few decades. It certainly seems to have progressed at a velocity that we’ve never experienced before in human history. Which makes it all a very very interesting topic on which to opine and philosophize. But the essence of the issue is all of us. It is you and me. It is our families. It is our friends. It is people we know. It is people that we don’t know. Millions of them. Dear reader, ours is a Human Problem. Not a math problem. But math tends to be what decides our fate. And so it is what we discuss.

For example, former Fed Chairman Paul Volcker is venerated and hailed as the hero who crushed inflation in the 1980s1. Volcker took his office and made policy and mortgage rates shot to over 18% and the wide world meekly went along. Yes, inflation abated. Volcker solved for X. He fixed the glitch. And today he is a hero because of it. But the real repercussions of Volcker’s policy were real consequences for real people. Average people. People just doing their best in a system that they did not control. Unknown and unnamed people lost jobs. People (like my parents) divorced under the stress and heavy weight of debt. Farmers lost farms. Some people, trapped by their decisions and circumstances and the shame of failure, committed suicide. These were not bad people. They were not doing bad things. They were just people making decisions in an uncertain world. Theirs is a story not told in the economic texts. Theirs is a story not reflected in the math. And now so many years past, they are mostly forgotten by most of us. But real people they were. And they also have a story to tell and lesson to share.

My point is only that we must remember that for all the discussion and math and philosophy, there is a human price to pay. We cannot be too theoretical, too mathematical, and therefore too glib about policy. Mr. Powell wants the labor market to cool. He wants unemployment to increase. He wants wages to, if not decrease, then at least not increase. So then to solve for X and decrease the boogeyman of inflation. But within this philosophy real people will suffer. Real people will lose (are already losing) their jobs and will go home to face families with nothing but questions and uncertainty. There will be real hurt there. And none of it will ever make the news. If Average Joe loses his job and house and chooses pills and disability over finding new work, he will only become a statistic in a book on demographics discussed on a podcast. Few will really care.

Sorry to preach. Please keep in mind that these ramblings are me sorting through my own thoughts? I think that my conclusion is something along the lines of count your blessings but not your chickens. Hold the ones you love close and cherish the now in spite of tomorrow. Invest wisely. Save for a rainy day. And do not hold on too tight spurious ideas of what might happen tomorrow. Life has a way of surprising us all.

The Curve Must Revert

Speaking of glib math, the curve must revert.

Our current Fed chairman cites Volcker as a sort of hero and influence. Jerome “Jay” Powell wants to be revered like him. But, dear reader, let us not forget that Paul Volcker stands atop a mountain of destruction.